When it comes to running a home service business, late payments, unpaid invoices, and untracked income can quickly disrupt your cash flow. This can leave you scrambling to figure out how you’ll pay for materials, supplies, or your employees.

Worrying about finances makes it harder to focus on growing your business, but there are simple changes you can make to simplify the way you keep track of your success.

In this article, we’ll show you how to keep track of invoices and payments with 5 easy tips, so you can boost your cash flow and keep your business thriving.

What is invoice management?

Before learning how to keep track of invoices and payments, let’s start with the basics: What is invoicing management?

Invoice management is the process of tracking all the invoices your business sends out. It involves creating, sending, and keeping records of invoices, as well as monitoring payments and following up on overdue invoices.

Essentially, invoice management is all about staying on top of your billing process to keep your business running smoothly.

Let’s take a look at 5 tips on how to keep track of invoices and payments.

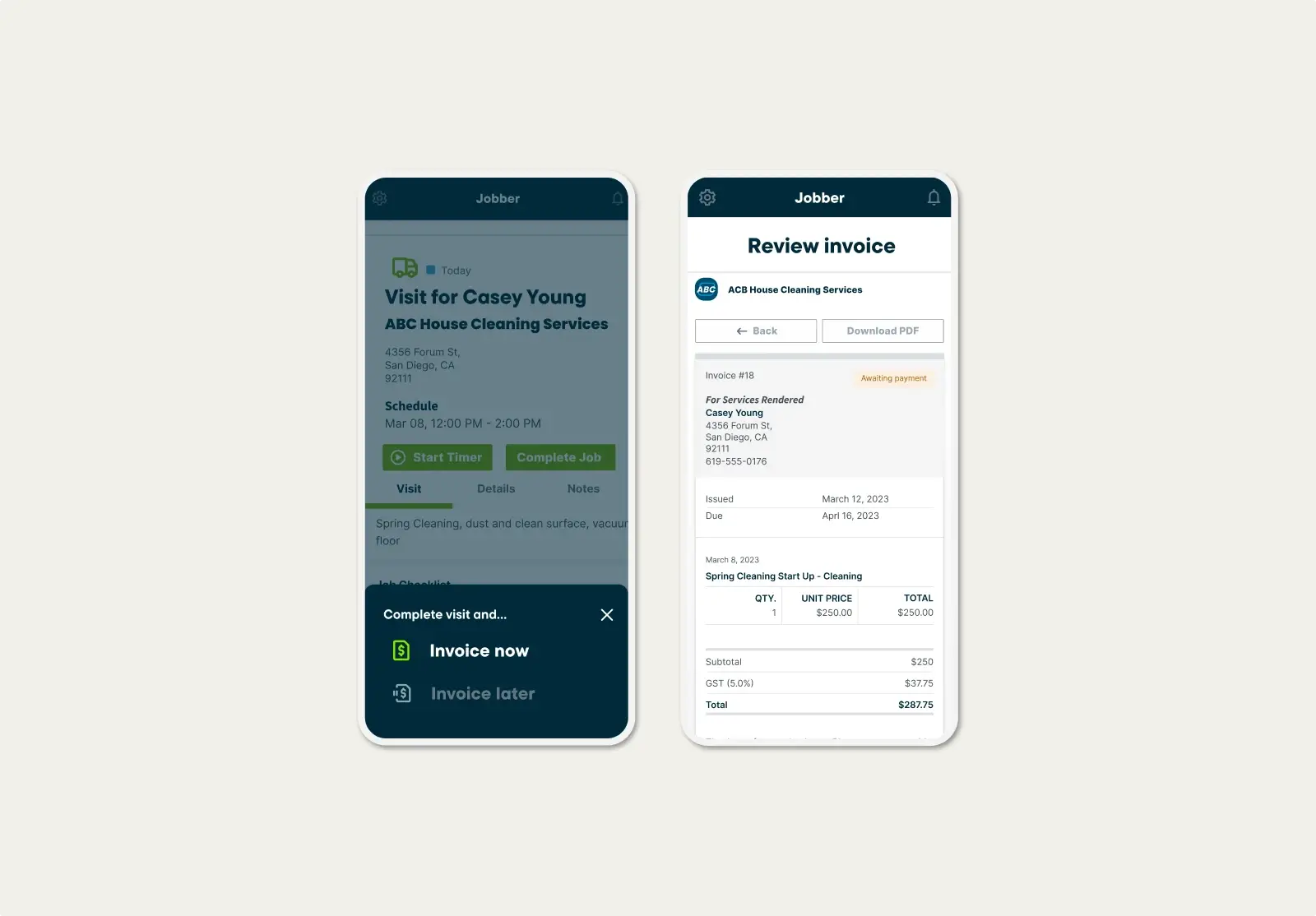

1. Send digital invoices

If you’re looking to make your invoicing process faster and easier, sending digital invoices is a no-brainer.

For starters, they’re quick to send, easy for your clients to pay, and you don’t have to worry about a paper invoice getting lost in a pile of mail.

Digital invoicing also makes tracking payments simpler. Everything is in one place and easily found in your records, especially if you’re using invoicing software.

Field service invoicing software such as Jobber lets you create invoices complete with your company branding, that can be sent to customers by text or email with just one click.

And if you’ve fallen behind on invoicing, or just prefer to send them all at once, batch invoicing can help. Simply select all the jobs you’d like to create invoices for, and send them to customers with a couple of clicks.

By using Jobber, you not only send invoices quickly, but you also keep them in one centralized location. This allows you to stay organized and easily pull up invoice numbers when you need them.

Pro Tip: Make sure your invoices have clear payment terms, including potential late fees. That way, you know that you have given your customer all of the information they need to make a timely payment.

READ MORE: What to include on an invoice

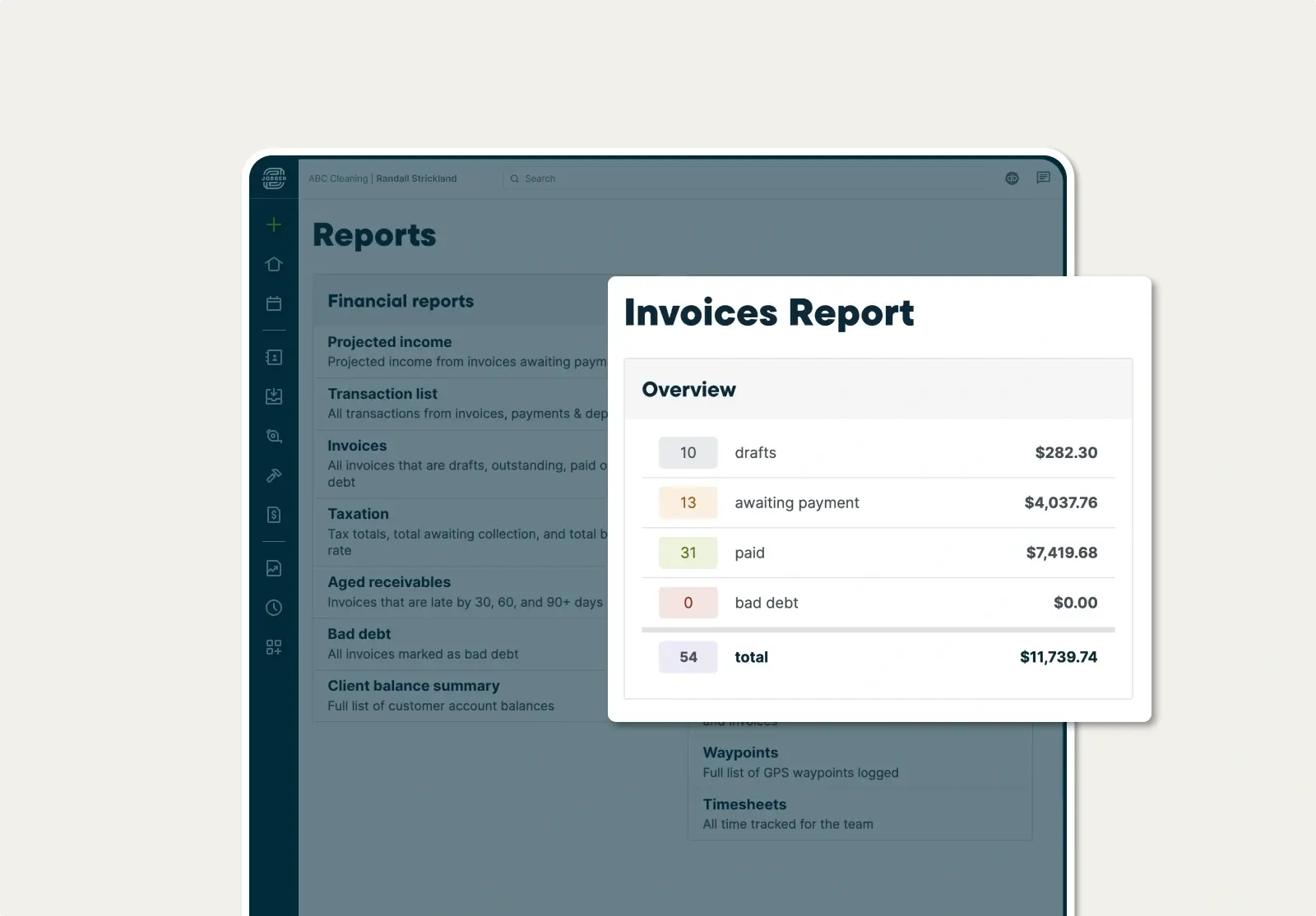

2. Make better decisions with regular reporting

Reports provide a consolidated view of all of your invoices and payments, making it easier to see what is outstanding, what has been paid, and what is overdue.

Regular reporting also provides visibility into the timing of payments. By knowing when invoices are due and when payments are expected to come in, you can manage your cash flow more effectively, helping with budgeting and forecasting.

Finally, reporting helps you identify patterns in payment behavior. You can track which customers are consistently late or which ones pay on time, which you can use to make better business decisions.

Jobber lets you access real-time data of all of your invoices. You can filter your reports by payment status so you can see your draft invoices, paid invoices, and outstanding invoices.

3. Pick the right accounting software

Good accounting software is key to an effective invoicing process, so it’s important to choose the right solution when figuring out how to keep track of invoices and payments.

QuickBooks Online is the best option for small businesses looking for more than invoice tracking software. QuickBooks allows you to manage all parts of your accounting that contribute to a seamless invoicing process, including accounts receivable, financial reporting, and receipt tracking.

READ MORE: How to write a receipt for your service business

For an even more powerful invoicing system, pair QuickBooks with Jobber for an all-in-one field service management solution. Automatically sync your invoices from Jobber to QuickBooks to eliminate double data entry for a smoother workflow.

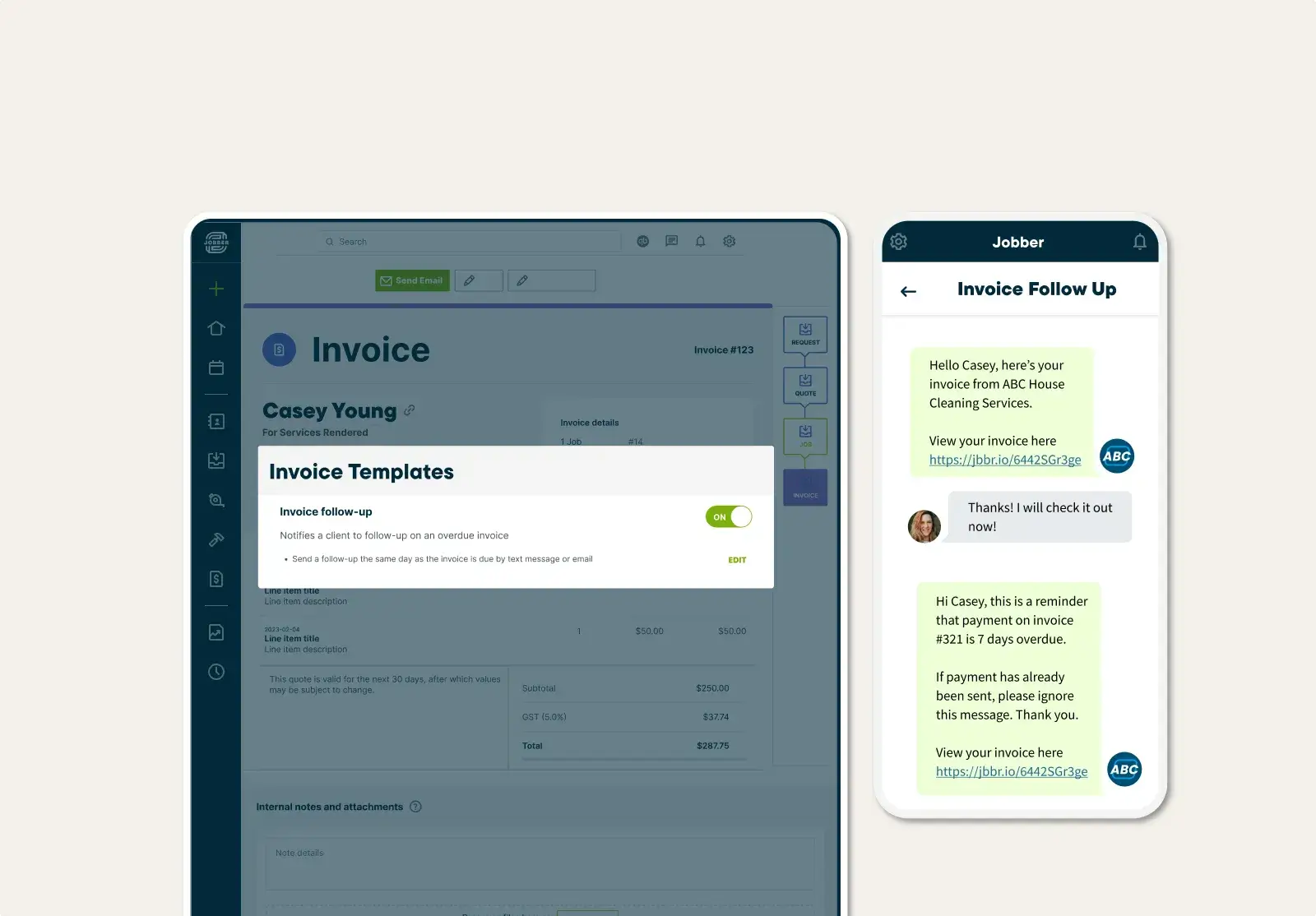

4. Streamline invoice tracking with automation

Keeping up with invoices and payments can feel like a heavy load, but leveraging automation through invoicing apps can relieve that burden. By automating certain tasks, you can track invoices and payments without lifting a finger.

Key invoicing tasks that you can automate include:

- Sending overdue payment reminders

- Recurring invoicing

- Credit card processing

Through automation, Jobber provides a better way to keep track of outstanding invoices. Use Jobber to set up automated invoice reminders on your calendar so you know when it’s time to invoice a job and when.

You can also set up Jobber to send automatic payment reminders to your customers for overdue payments to avoid awkward phone calls.

We send payment reminders through Jobber as a polite, professional way to remind our customers that payment is due and to call us if there are any concerns.

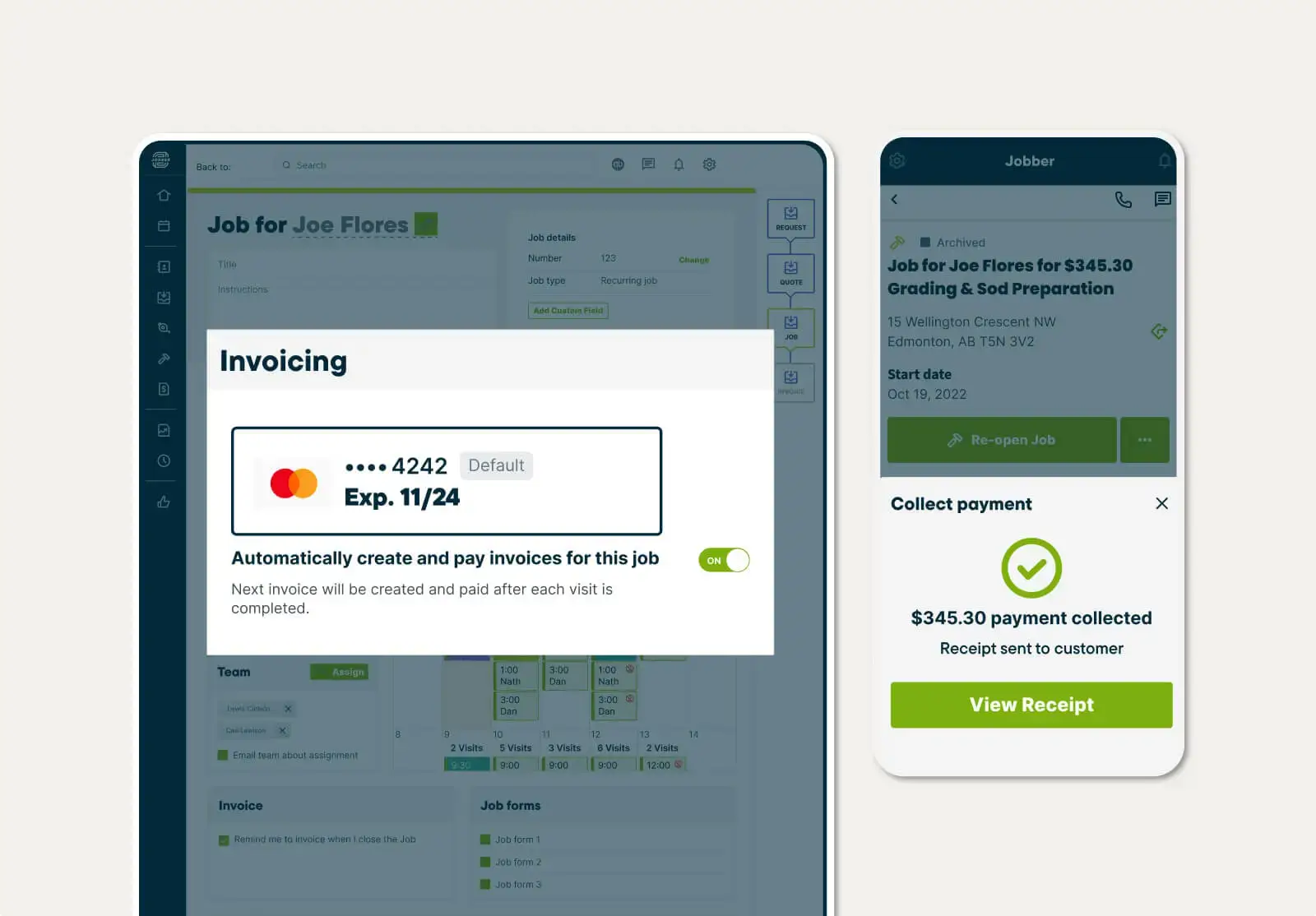

5. Accept credit card payments

Providing multiple payment methods, such accepting credit card payments, can give your cash flow a noticeable boost and make it easier to track payments as they come in.

With Jobber’s Online Payments, you can offer customers convenient online payment experiences they’ve come to expect from businesses. Customers can easily pay their invoice online through the client hub using their debit or credit card.

For recurring payments, Jobber can automatically charge credit cards saved on file, ensuring that invoices get paid on time, every time.

Learning how to keep track of invoices and payments doesn’t have to be a headache. With the right tools and a bit of automation, invoice tracking can be a smooth process that leaves you with more time to focus on what you love about your business.

Frequently Asked Questions

-

Depending on your business, your home service techs could be handing invoices and even collecting payment before they leave the customer’s home. That’s why it’s important to have an organized system to track your invoices.

Tracking invoices and payments helps keep your cash flow in check and ensures you get paid on time. With solid system in place, you can:

1. Save time on invoice processing

2. Avoid late payments

3. Prevent misunderstandings with clients

All of this keeps your home service business running smoothly. Plus, it gives you a clear picture of your income, helping you plan better for the future and grow your business without the stress of financial guesswork.

-

Use invoice tracking software such as Jobber to automate the way you handle invoices and payments, stay organized, and save time.

Use Jobber to:

– Generate and send professional invoices in minutes

– Get notified when it’s time to send an invoice

– Send multiple invoices at once in just a few clicks

– Automatically send customized email or text follow ups for outstanding payments

READ MORE: How to write an invoice -

Keep track of your paid and unpaid invoices by using an invoicing tool that organizes everything in one place.

The best invoicing solutions will automatically mark invoices as “paid” as soon as payment comes in to reduce manual work. -

Human error—such as misplaced invoices or incorrect data entry—is the biggest risk that comes with manually tracking invoices and payments. It can lead to missed payments and delayed cash flow.

Plus, managing everything on paper or spreadsheets can be time-consuming and disorganized, making it hard to find what you need when you need it. These factors can add unnecessary stress and costs to your business, so it’s important to consider more efficient tracking methods.