Jobber Home Service Economic Report

2024 Q3 | November 2024

Introduction

Small businesses employ 61.7 million Americans, totaling 46.4% of private sector employees1. As the leading software for Home Service businesses, Jobber is uniquely positioned to identify aggregate trends and insights in this important small business segment. More than 250,000 residential cleaners, landscapers, HVAC technicians, and more, keep track of jobs and charge their customers for work using Jobber.

Early stages of the interest rate cut are starting to influence consumer spending, signaling a gradual yet positive turnaround for the sector.

While the first half of 2024 has been a slow start for home services, we are starting to see momentum at the end of Q3. There is optimism around market conditions improving for the category as monetary policies ease, providing consumers with greater financial flexibility.

In this Jobber Home Service Economic Report, we will provide an update on consumer demand and housing trends as of Q3 and take a deeper look at the segments that make up Home Service, including Green, Cleaning, Contracting, and Construction.

Key takeaways:

- Interest rate cuts have begun positively affecting consumer spending and demand for home services.

- Consumer spending continued to increase, outpacing goods, despite mixed results in new work being scheduled.

- Median revenue remained steady, driven by larger average invoices, indicating a robust demand for services.

- Home equity values rose due to lower interest and mortgage rates, boosting investment in home improvements.

- Although growth in new work scheduled in the Green segment slowed in Q3, steady median revenue reflects a focus on smaller, recurring outdoor services.

- The Cleaning segment saw persistent scheduling fluctuations, but median revenue growth was held through strategic pricing and premium services.

- Contracting saw stable median revenue despite a late-quarter slowdown, as the focus shifted to high-value, complex projects.

- Construction saw median revenue improving as consumers prioritized maintenance over large construction projects.

- Expected rate cuts and financial conditions should increase home improvement spending through 2025.

- Aging housing stock is likely to maintain demand for home services as consumers prioritize necessary upgrades amidst economic uncertainty.

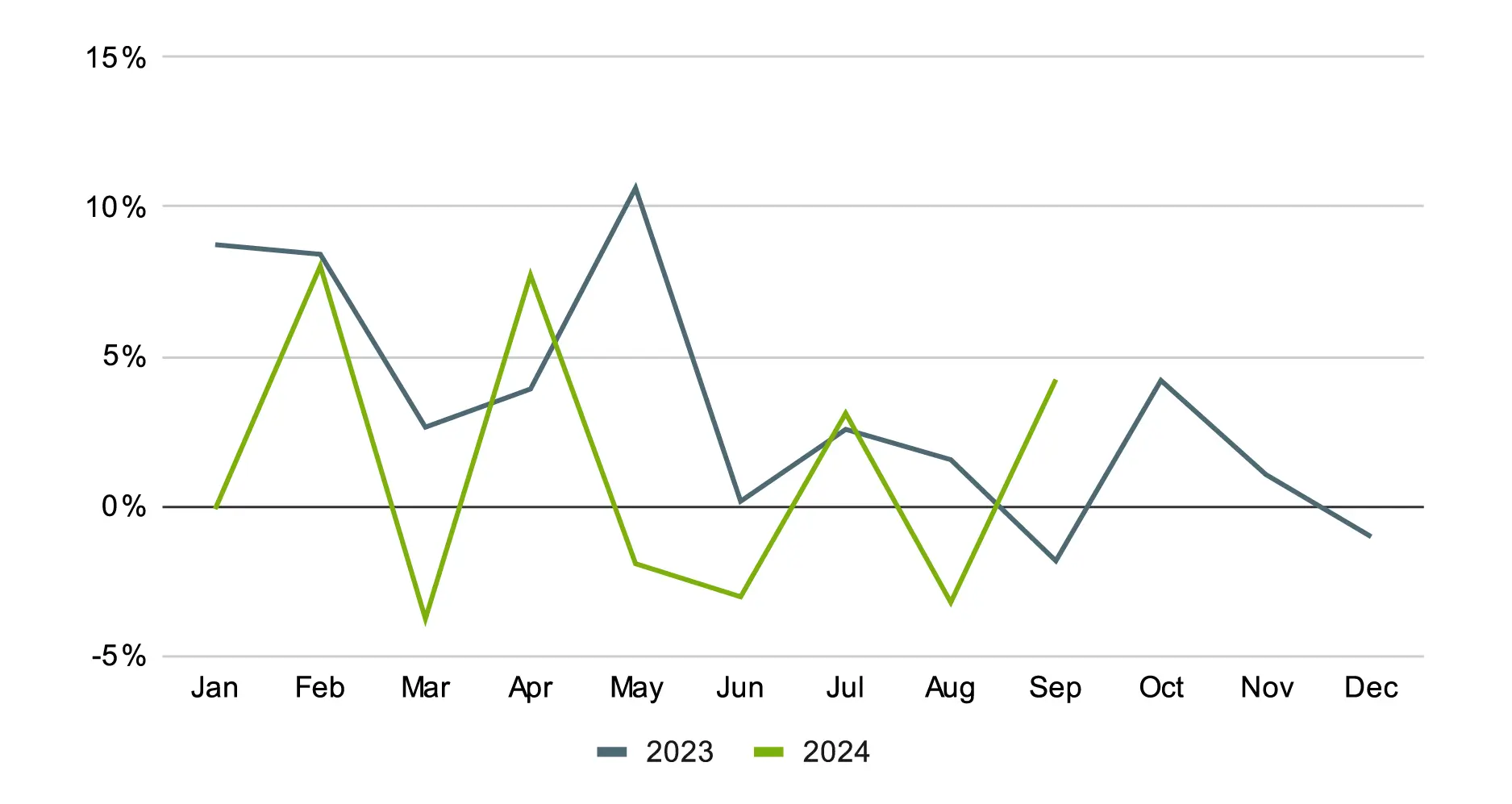

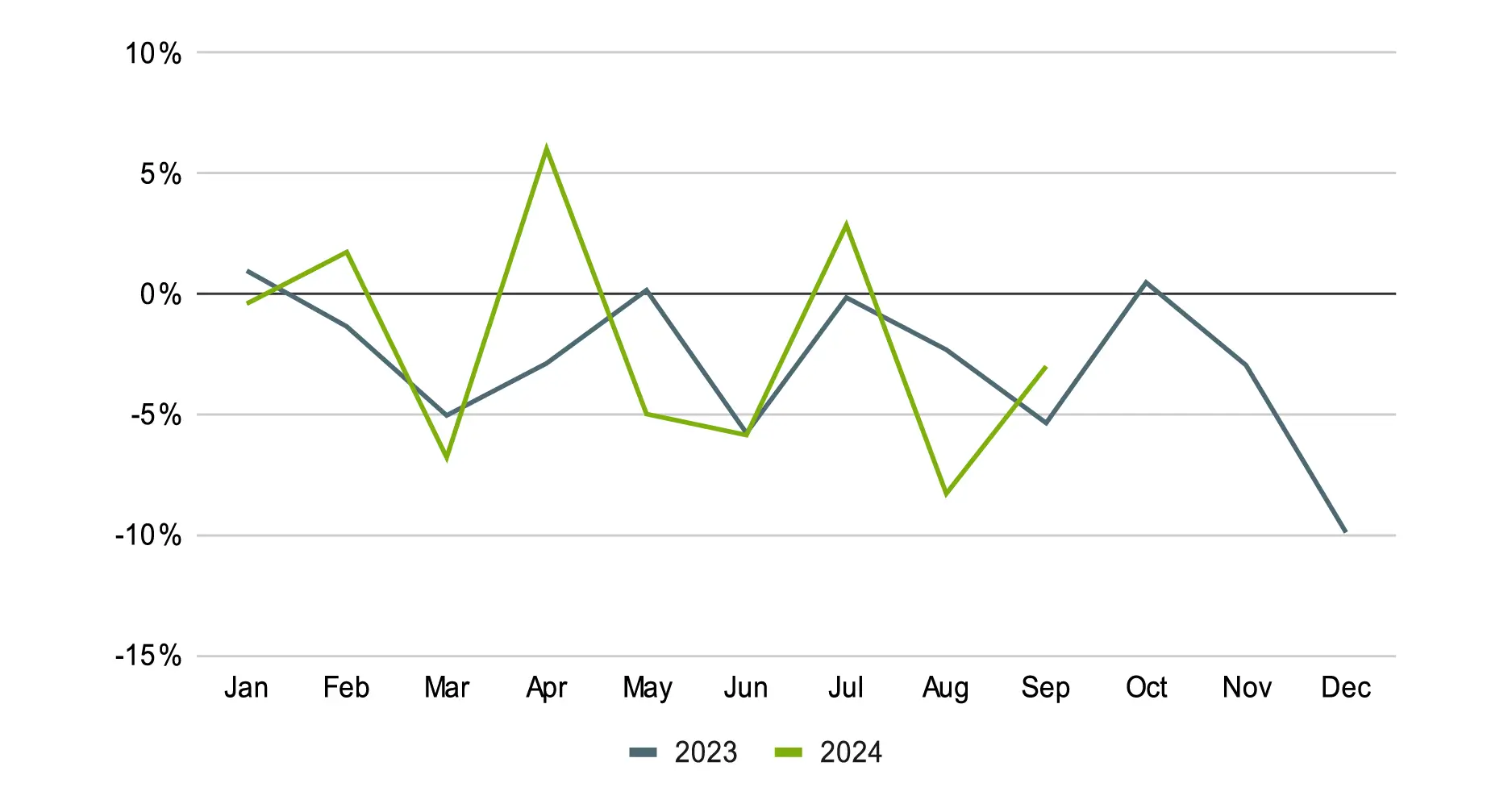

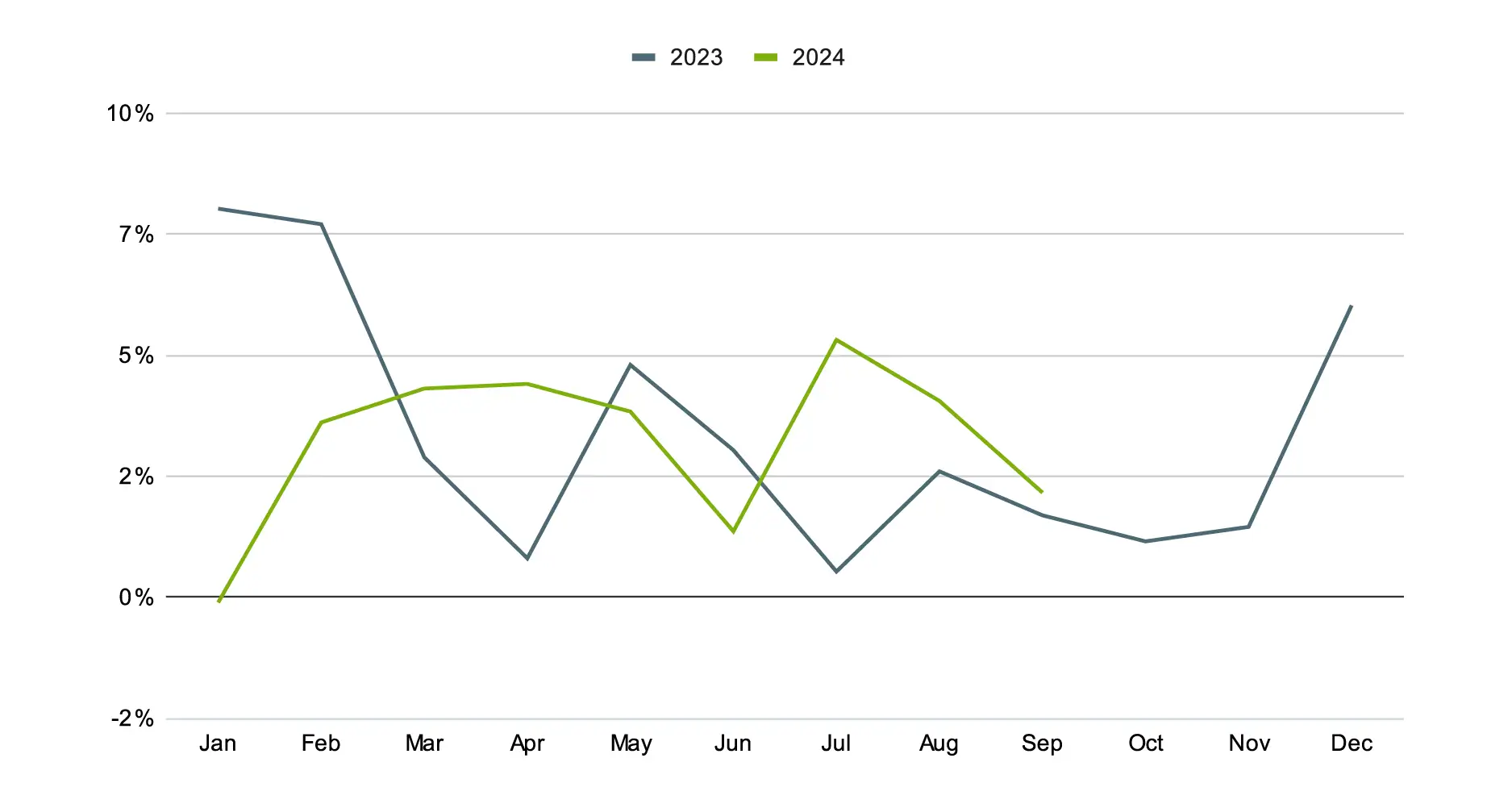

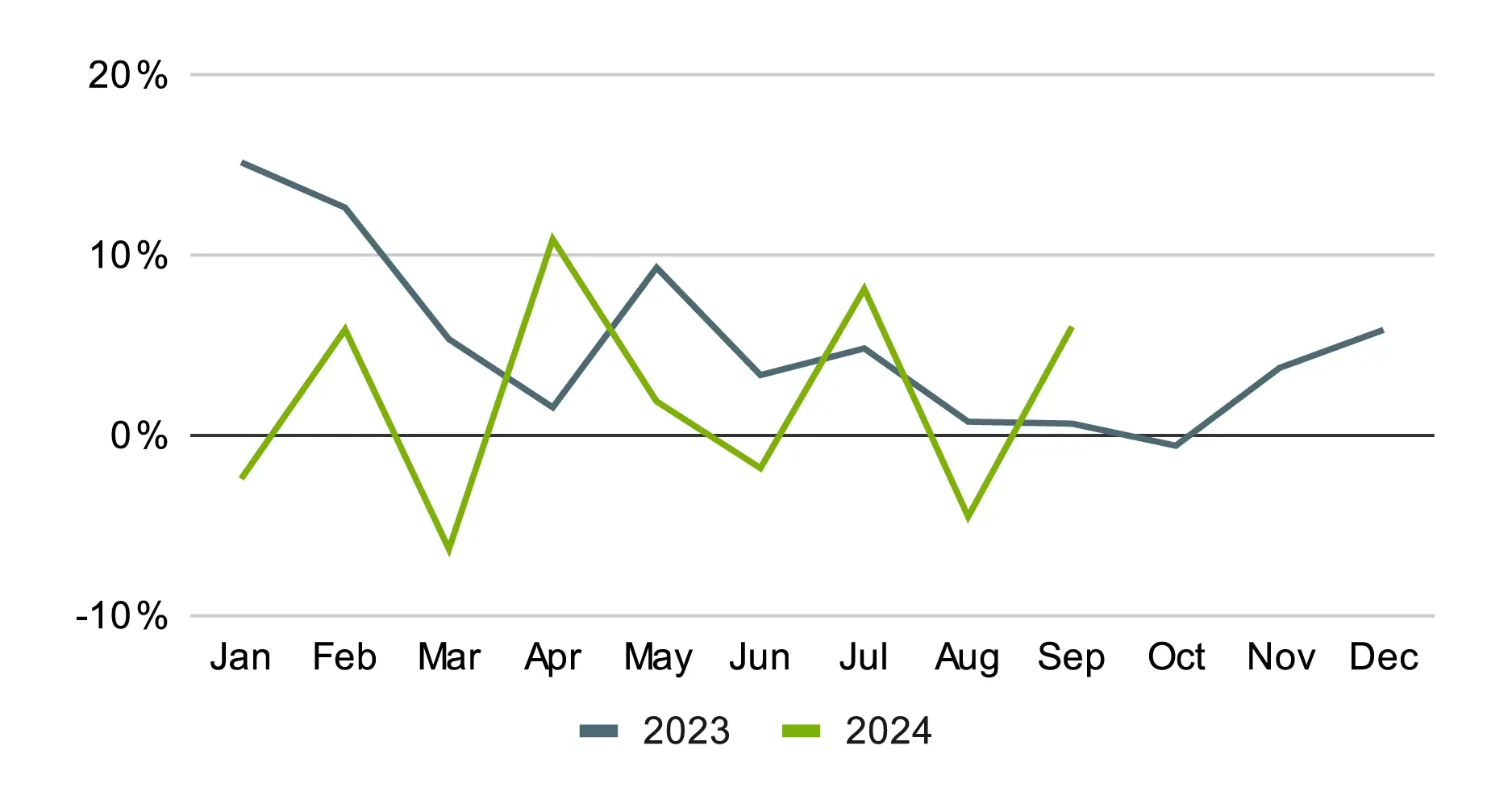

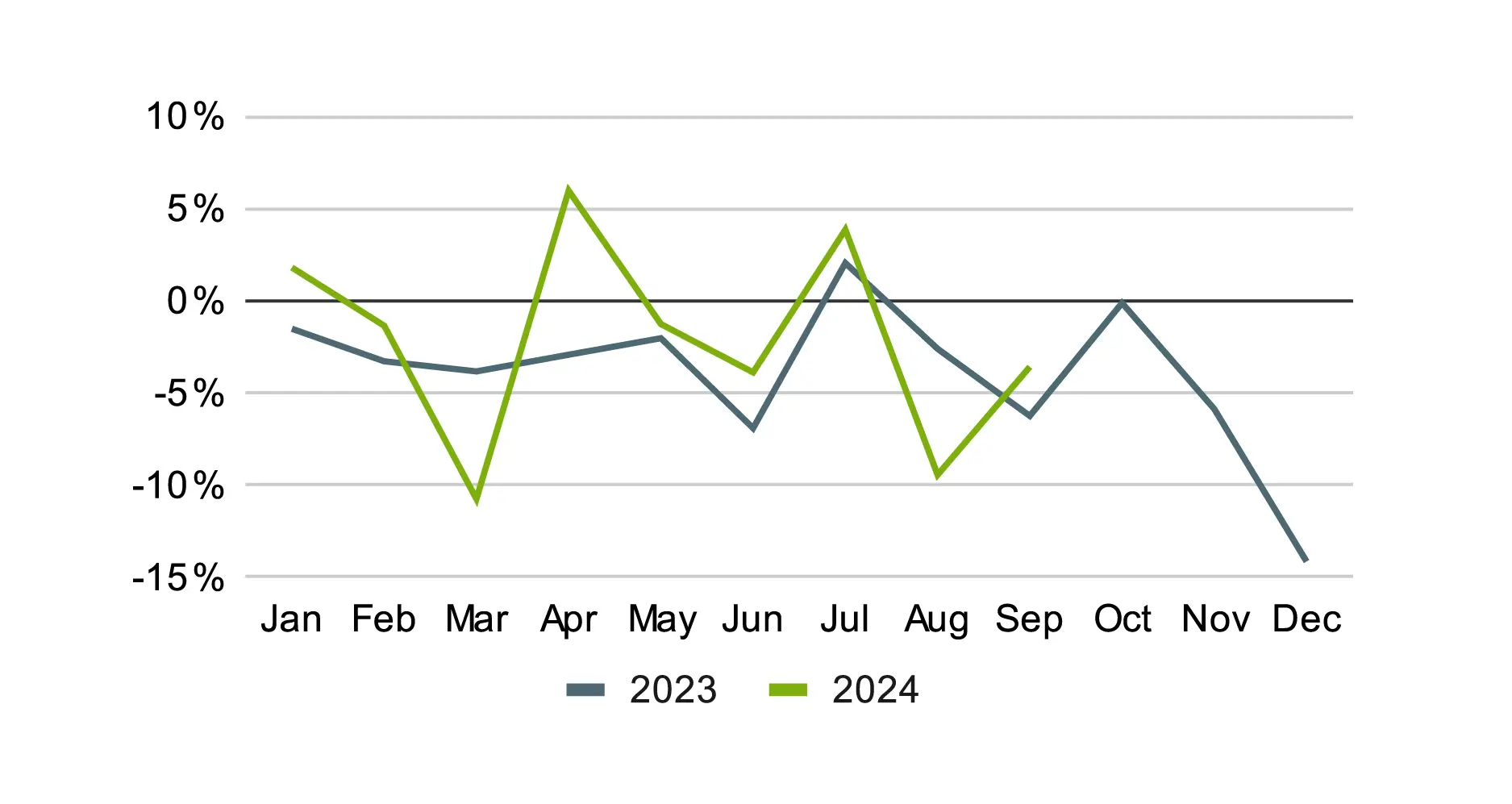

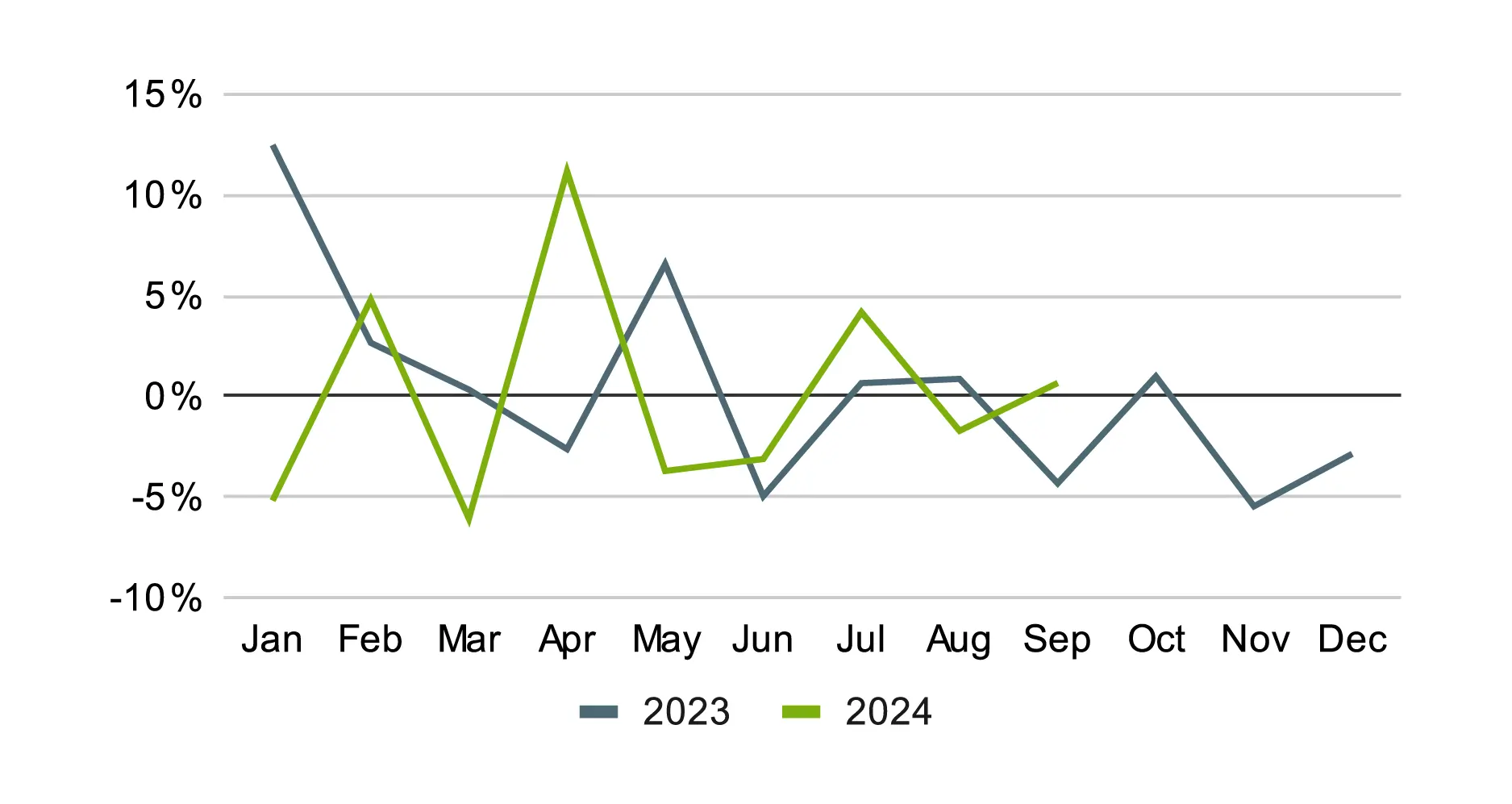

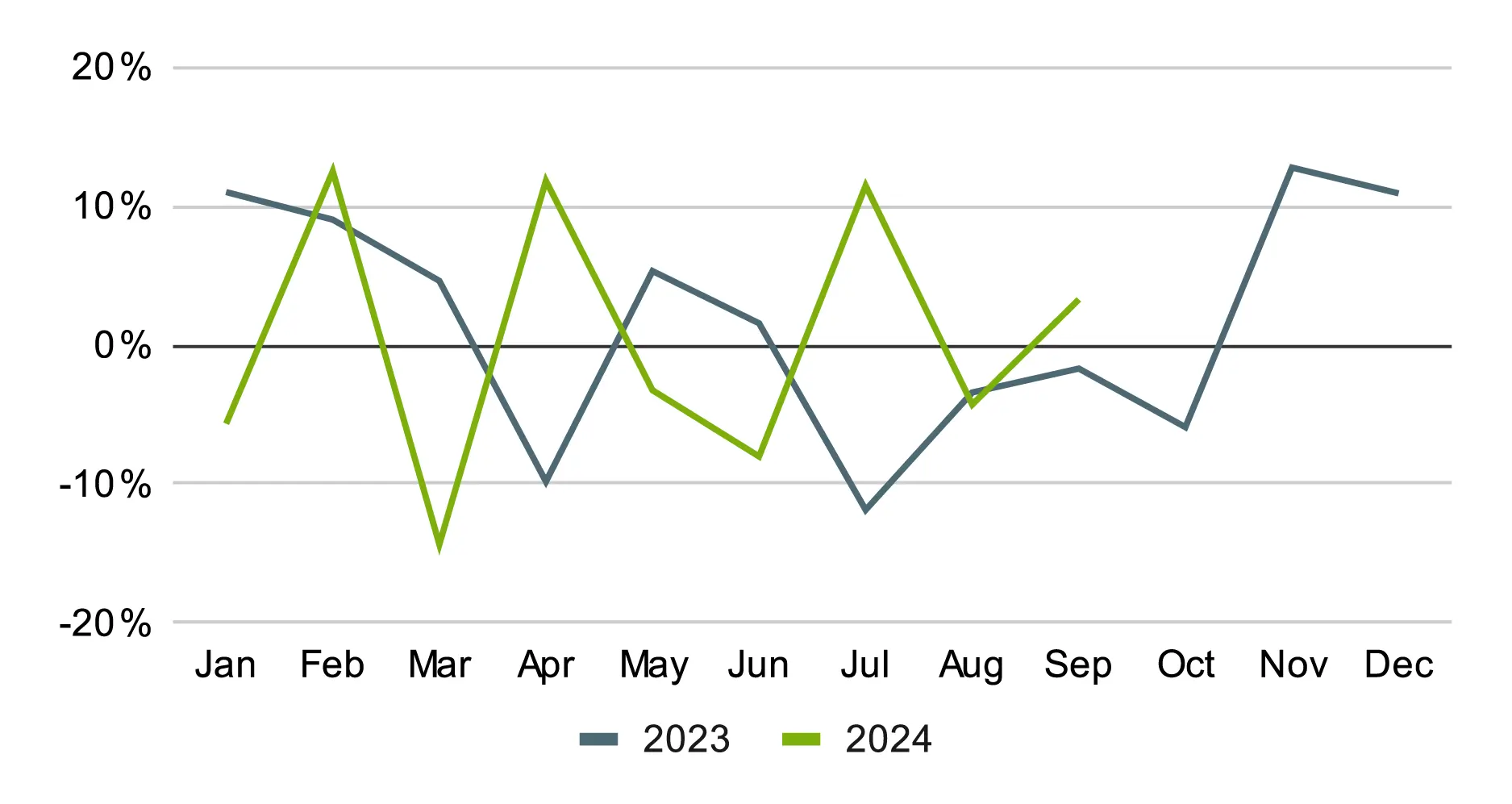

Consumer Demand

Overall, consumer demand remained resilient in Q3, with spending on services outpacing consumer goods2, helping to sustain steady revenue growth. Rising average invoice sizes have kept median revenue afloat despite the variability in new work scheduled. The seasonal increase in July—partly due to additional business days—helped offset some of the slower months.

Median Revenue YoY

New Work Scheduled YoY

Average Invoice Size YoY

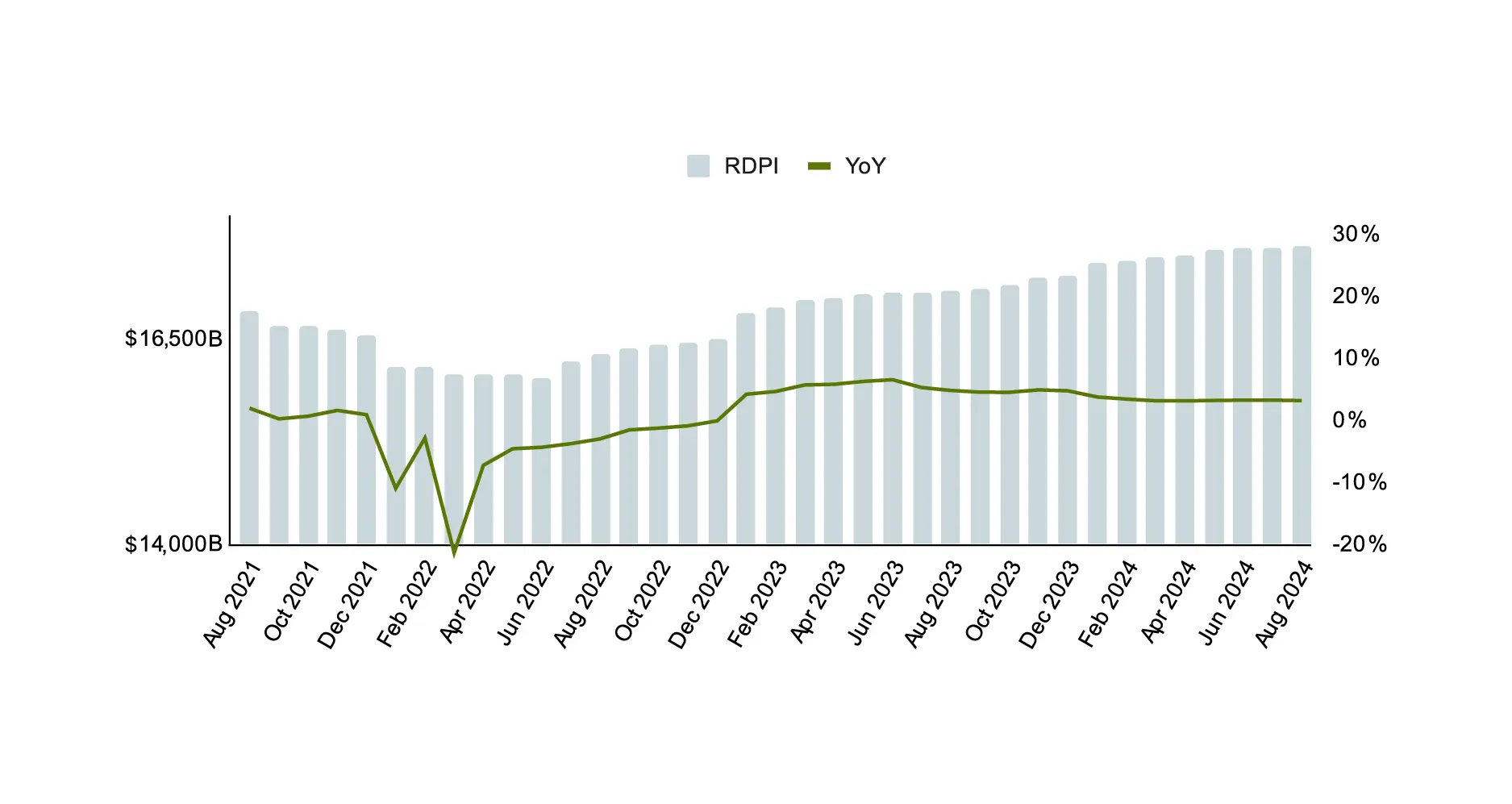

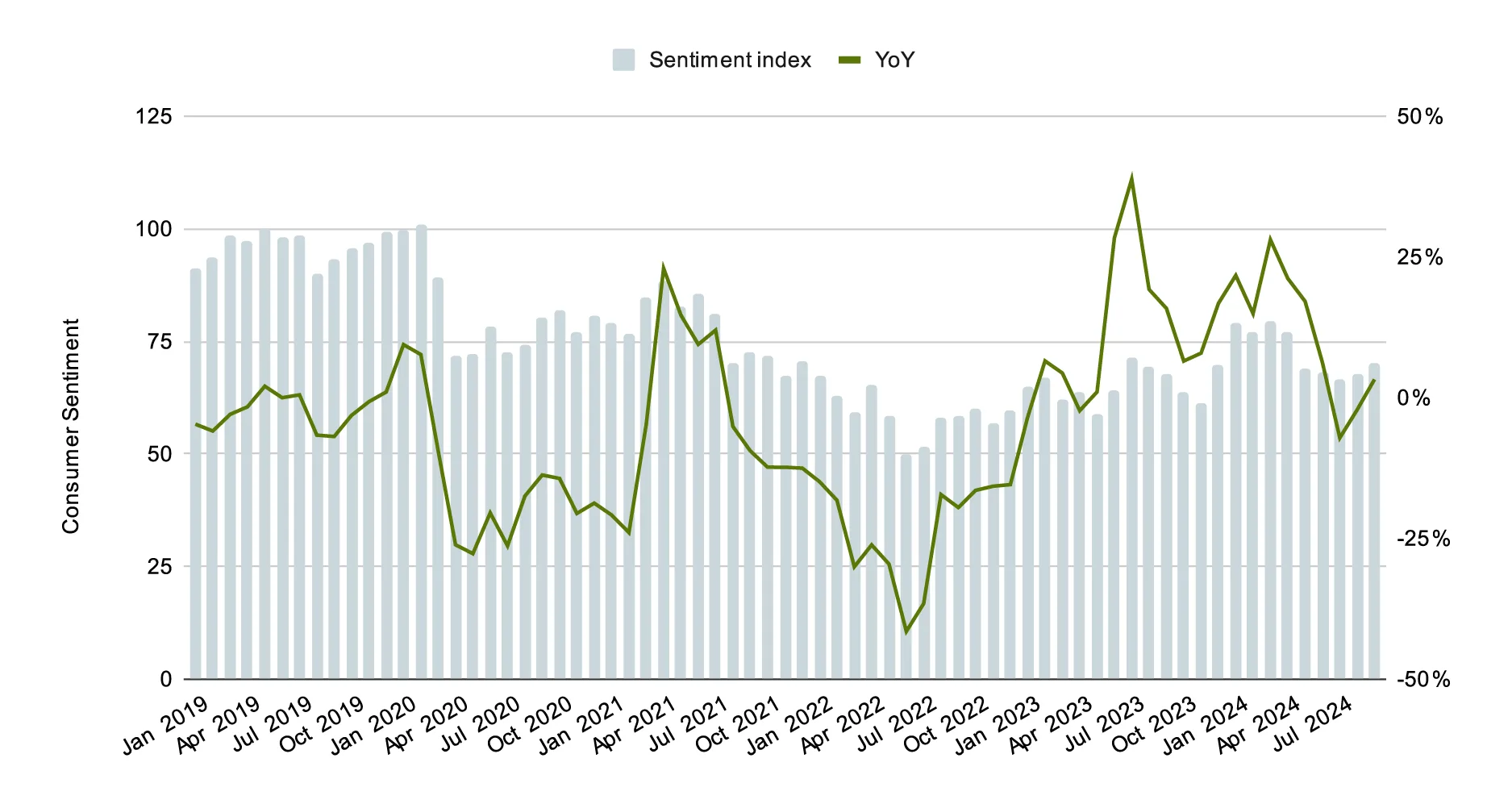

With the US Federal Reserve’s interest rate cuts announced last month, we are starting to see the early-onset effects on household income and consumer sentiment. Real Disposable Income3, or the amount of income left to spend after paying taxes, adjusted for inflation, stabilized at ~3% in Q3, improving consumer sentiment3 on the economy and boosting household spending flexibility.

Experts predict the interest rate-cutting cycles will continue well into 2025. In combination with falling inflation, we anticipate a positive impact on the housing market and home service sector. Accessibility to lower mortgage rates and more affordable financing for home improvement projects are expected to drive increased activity in both home buying and renovations.

Real Disposable Income ($Billions)3

Index of Consumer Sentiment YoY4

Housing Market: Positive Future Outlook

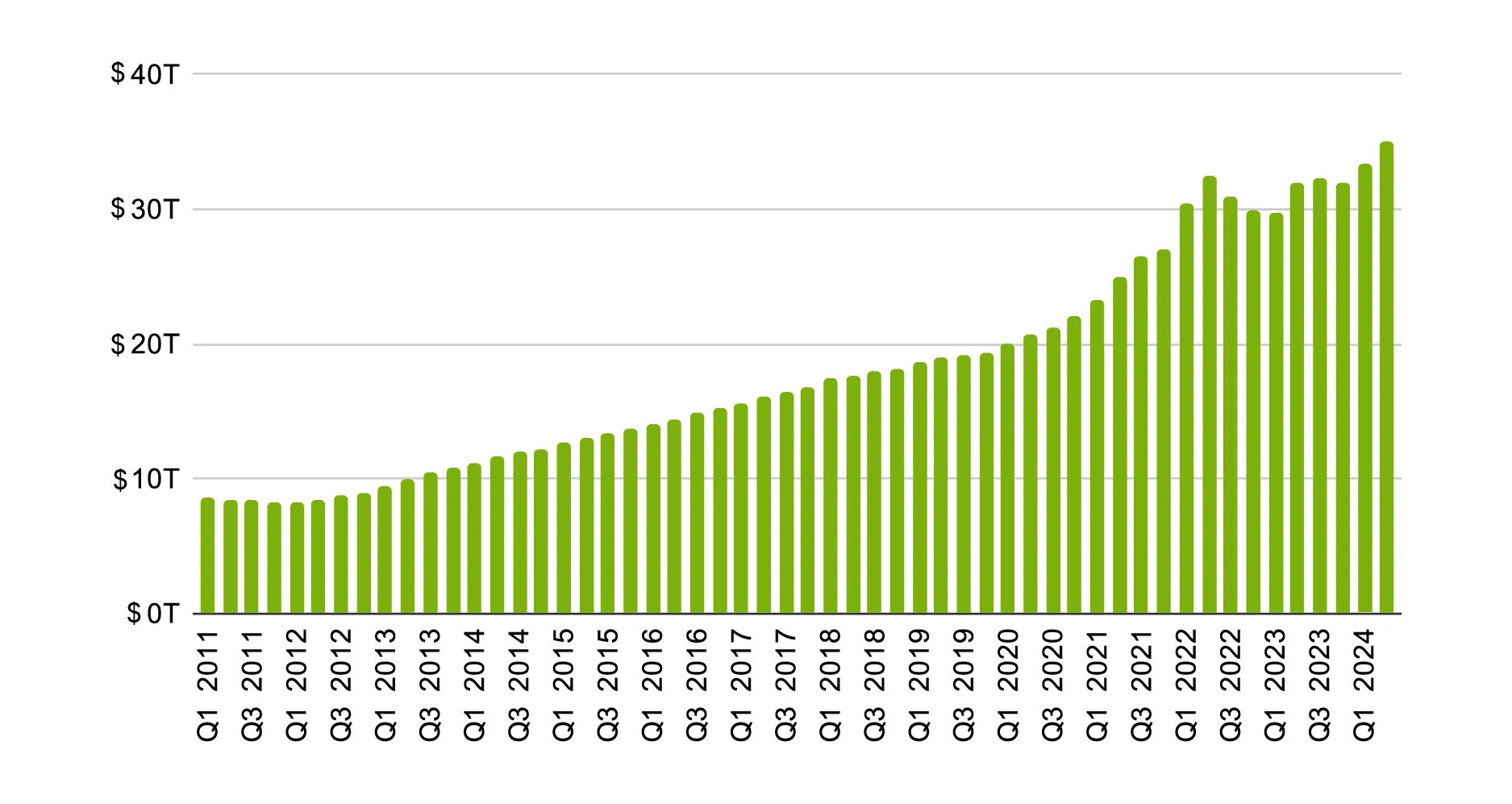

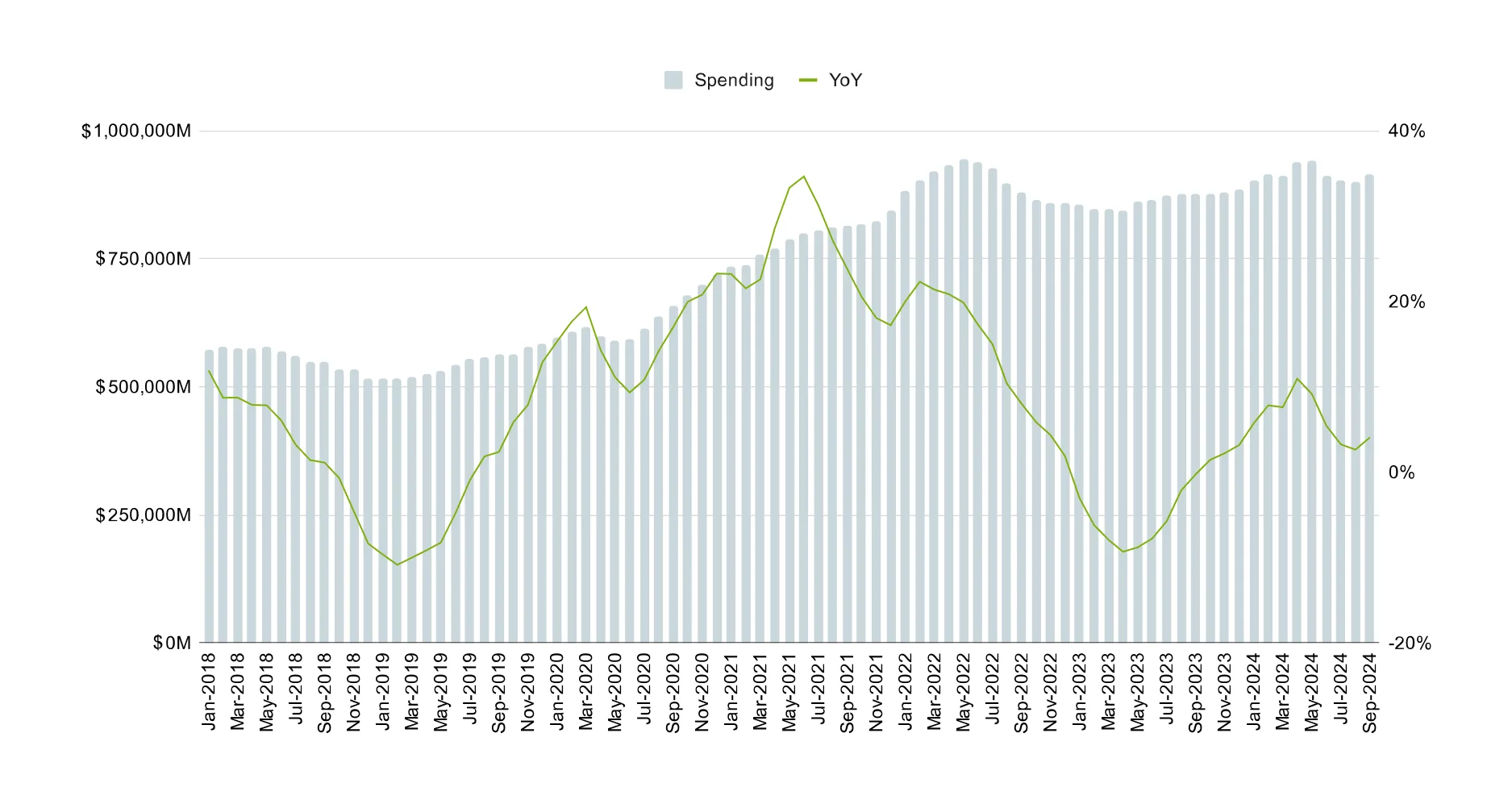

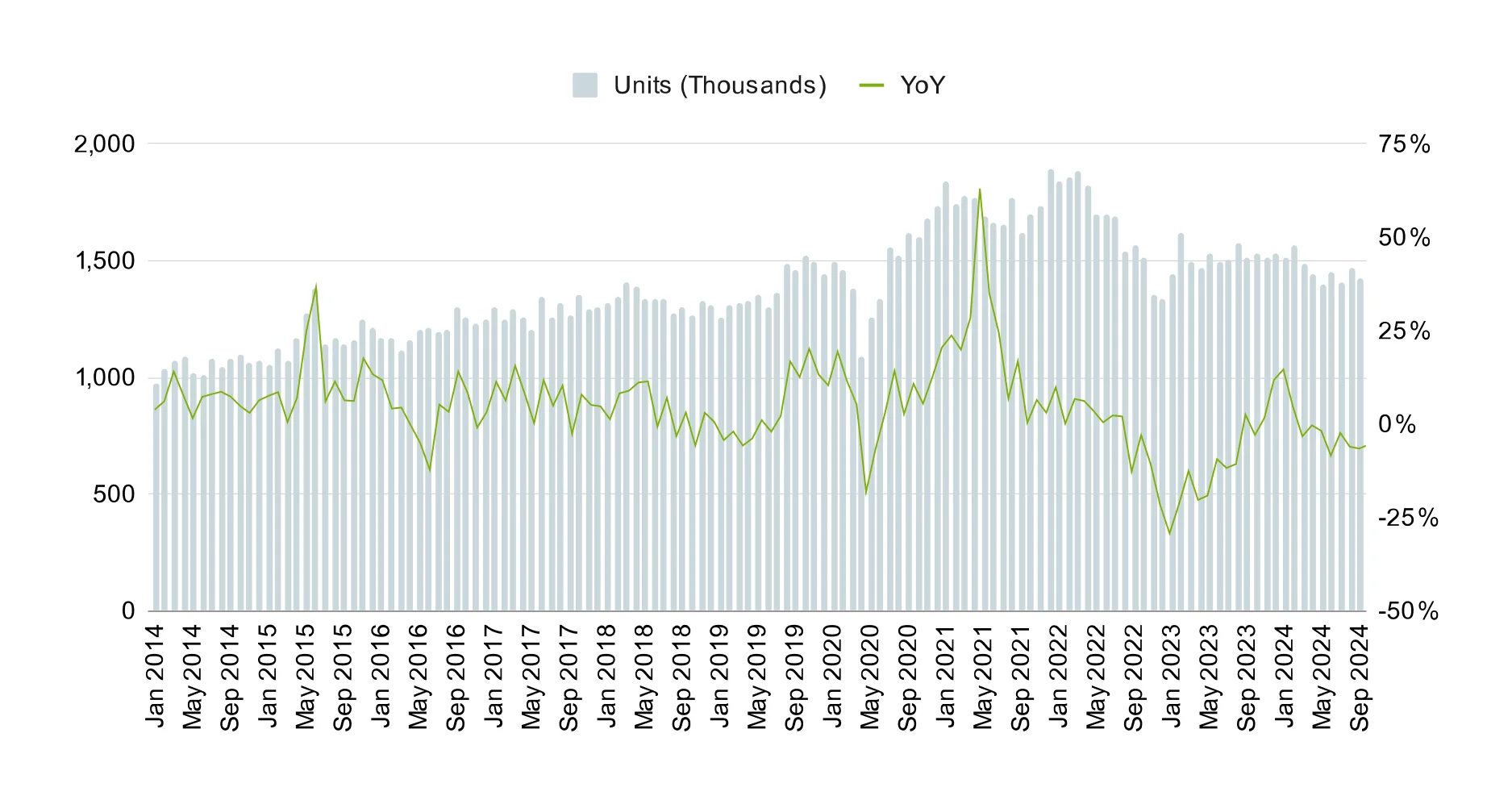

The performance and activity of the housing market are closely linked to demand for home services. Home equity values5 continued to rise and show no signs of slowing down as interest rate cuts helped to drive housing demand and multi-decade-high mortgage rates6 have started to come down. While monthly construction spending7, new permits8, and housing starts9 have started to stagnate, the cumulative effect of rate cuts is expected to renew activity in the market by mid-2025.

Home Equity Value ($Trillions)5

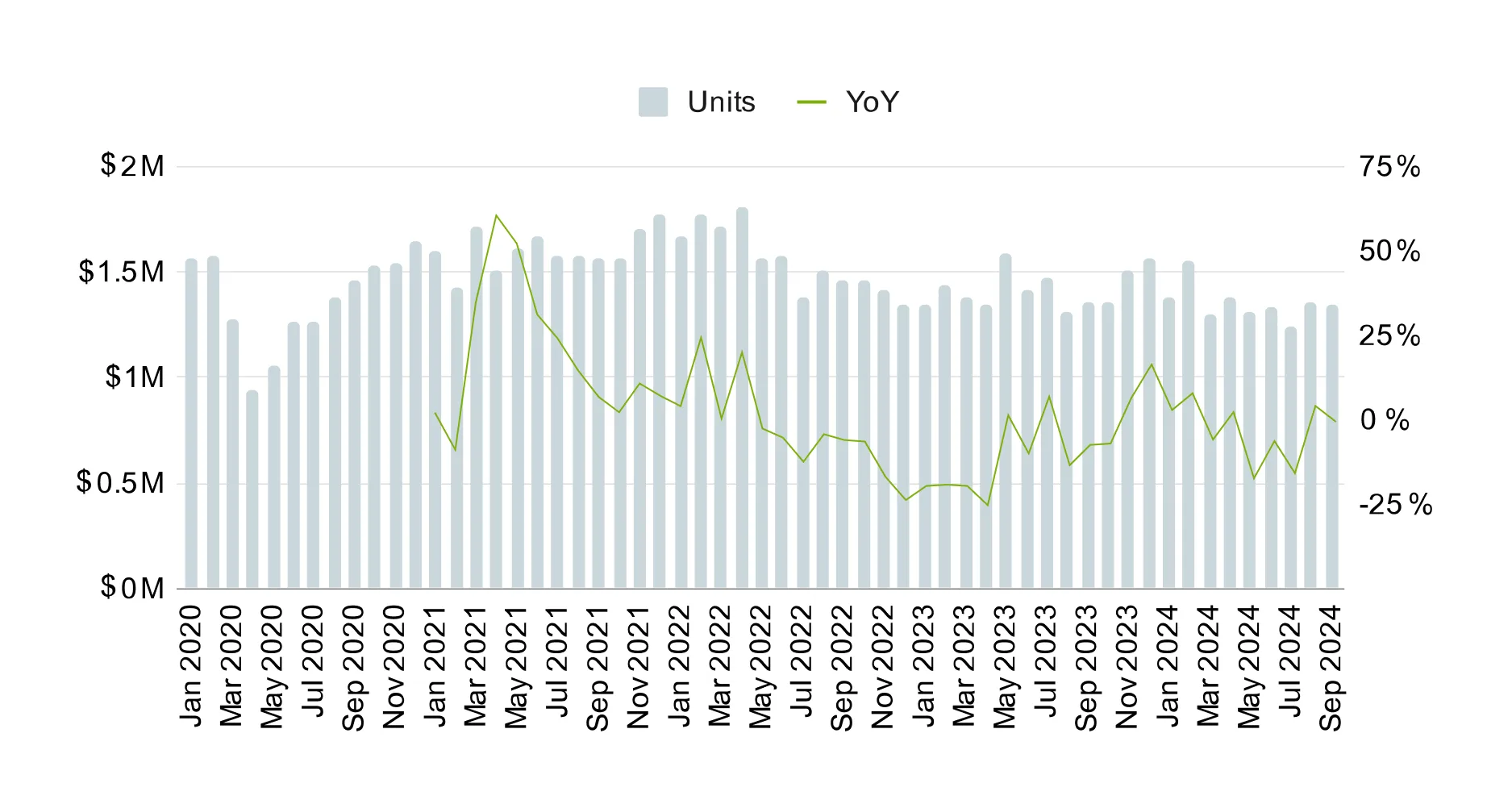

Monthly Construction Spend ($Millions)7

Average 30 yr Fixed Mortgage Rate6

Housing Permits YoY8

Housing Starts YoY ($Millions)9

After a brief slowdown, spending on home improvements and repairs for owner-occupied homes is expected to rise by mid-2025, according to Harvard’s Remodeling Futures Program10. Increased new home construction, home sales, and rising home equity will drive demand for both discretionary and mandatory projects. Annual spending is projected to increase from $472 billion to $477 billion by Q3 2025, approaching previous peak levels.

Home Service Category Performance

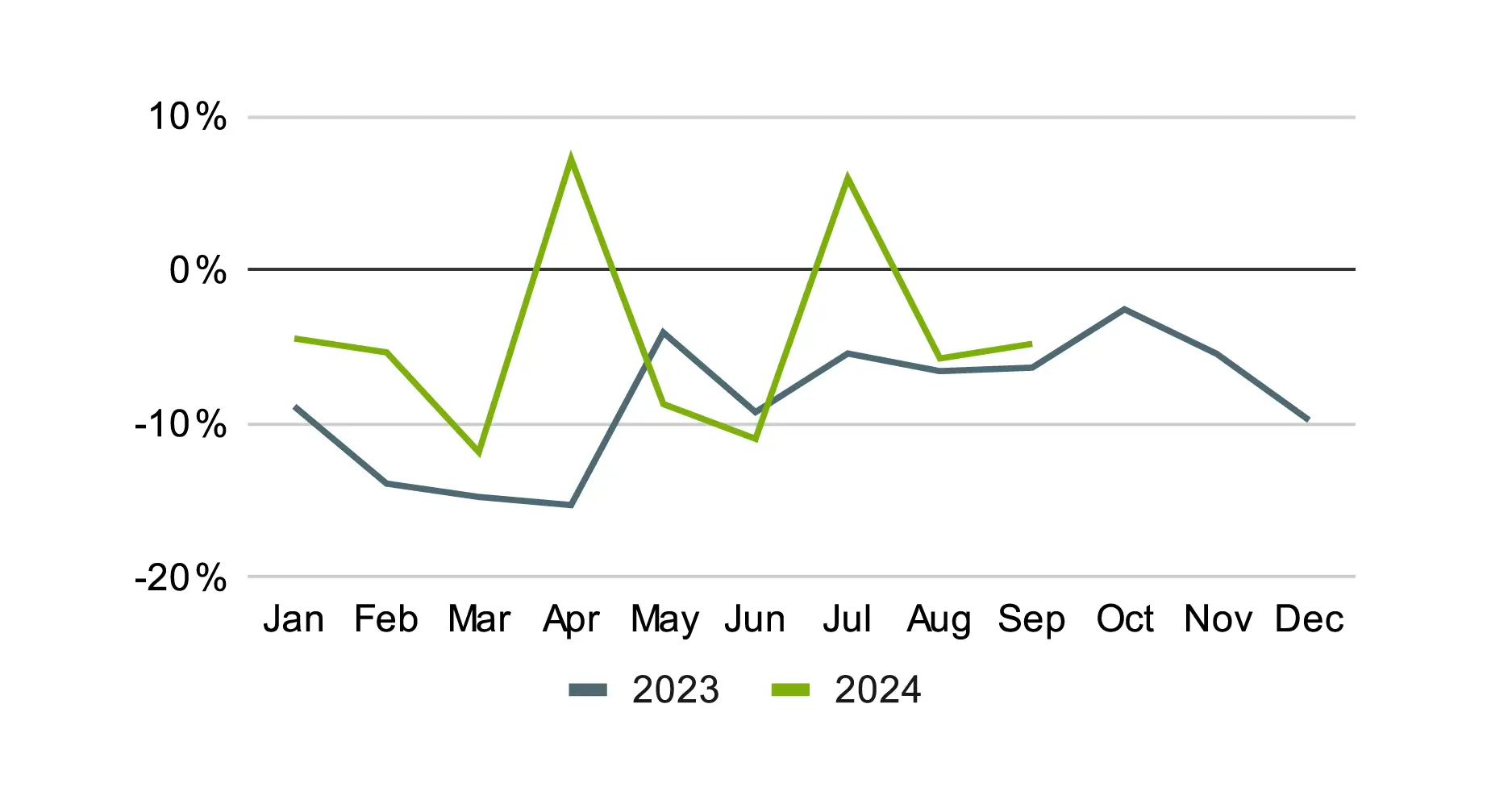

Green

The Green segment includes lawn care, landscaping, and other related outdoor services. There was a mixed outlook for this category—while new work scheduled saw growth early in 2024, it slowed down in Q3, with the exception of July. However, median revenue remained steady, reflecting homeowners’ continued investment in smaller, recurring services despite broader economic pressures. Although consumers are cutting back on large renovations, they still prioritize outdoor maintenance, aligning with the broader trends of maintenance.

New Work Scheduled YoY — Green

Median Revenue YoY — Green

Cleaning

Cleaning services encapsulate residential and commercial cleaning, carpet cleaning, junk removal, and other similar services. The updated Q3 data reveals an ongoing trend of rising median prices alongside declining volume within the category. New work scheduled followed a similar pattern in 2023, fluctuating every few months, reflecting the discretionary nature of many cleaning services as consumers pull back on spending. Despite these declines, service providers have managed to keep median revenue growth relatively stable, credited to price increases and a focus on premium services.

New Work Scheduled YoY — Cleaning

Median Revenue YoY — Cleaning

Contracting

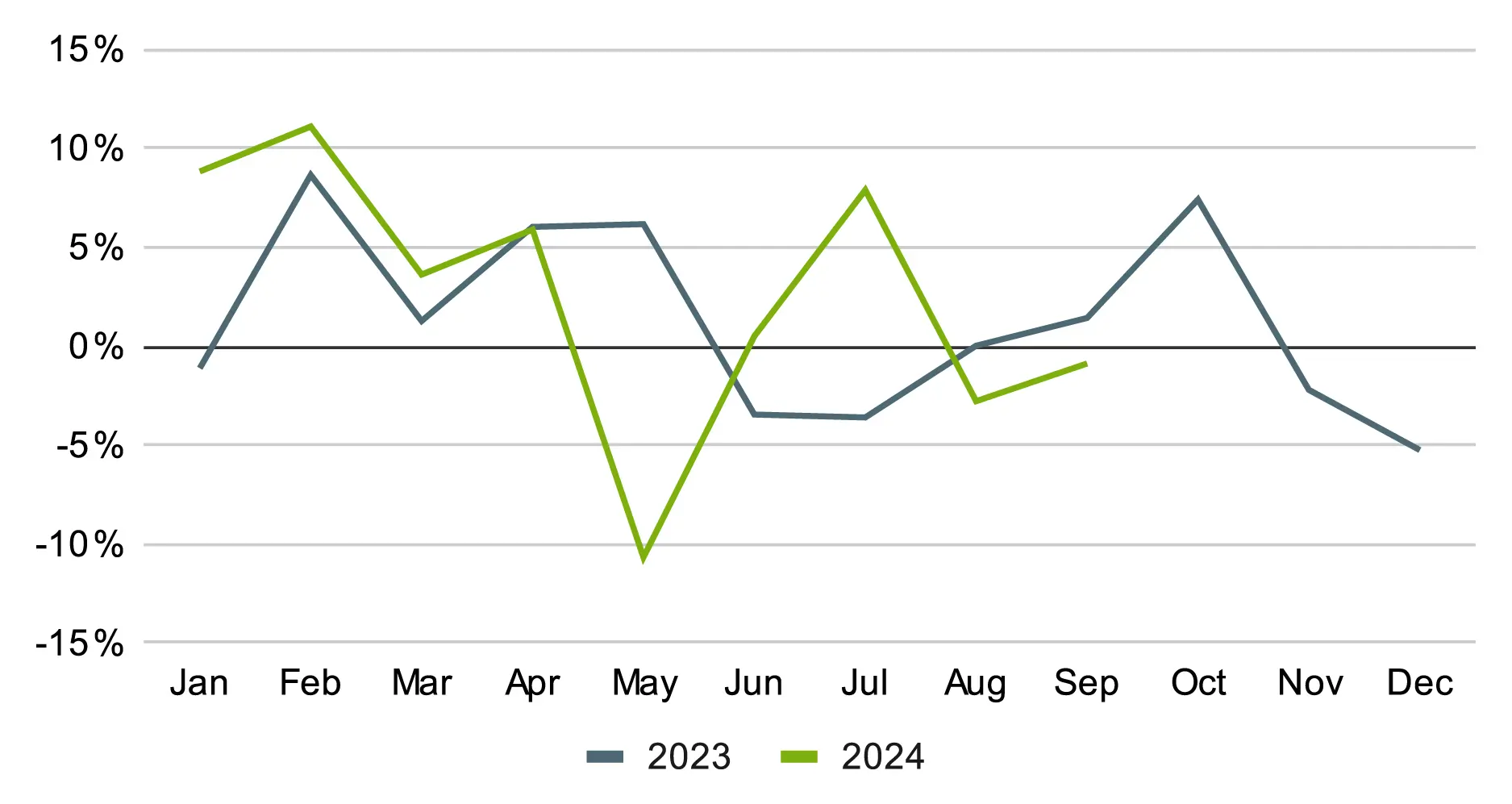

The Contracting segment includes arborists, electricians, handymen, HVAC, plumbers, and other non-construction contractor services. Q3 saw a downturn in new work scheduled towards the end of the quarter. However, median revenue growth has remained relatively flat, suggesting that pricing adjustments and possibly more complex or higher-ticket projects have helped offset scheduling variability.

New Work Scheduled YoY — Contracting

Median Revenue YoY — Contracting

Construction

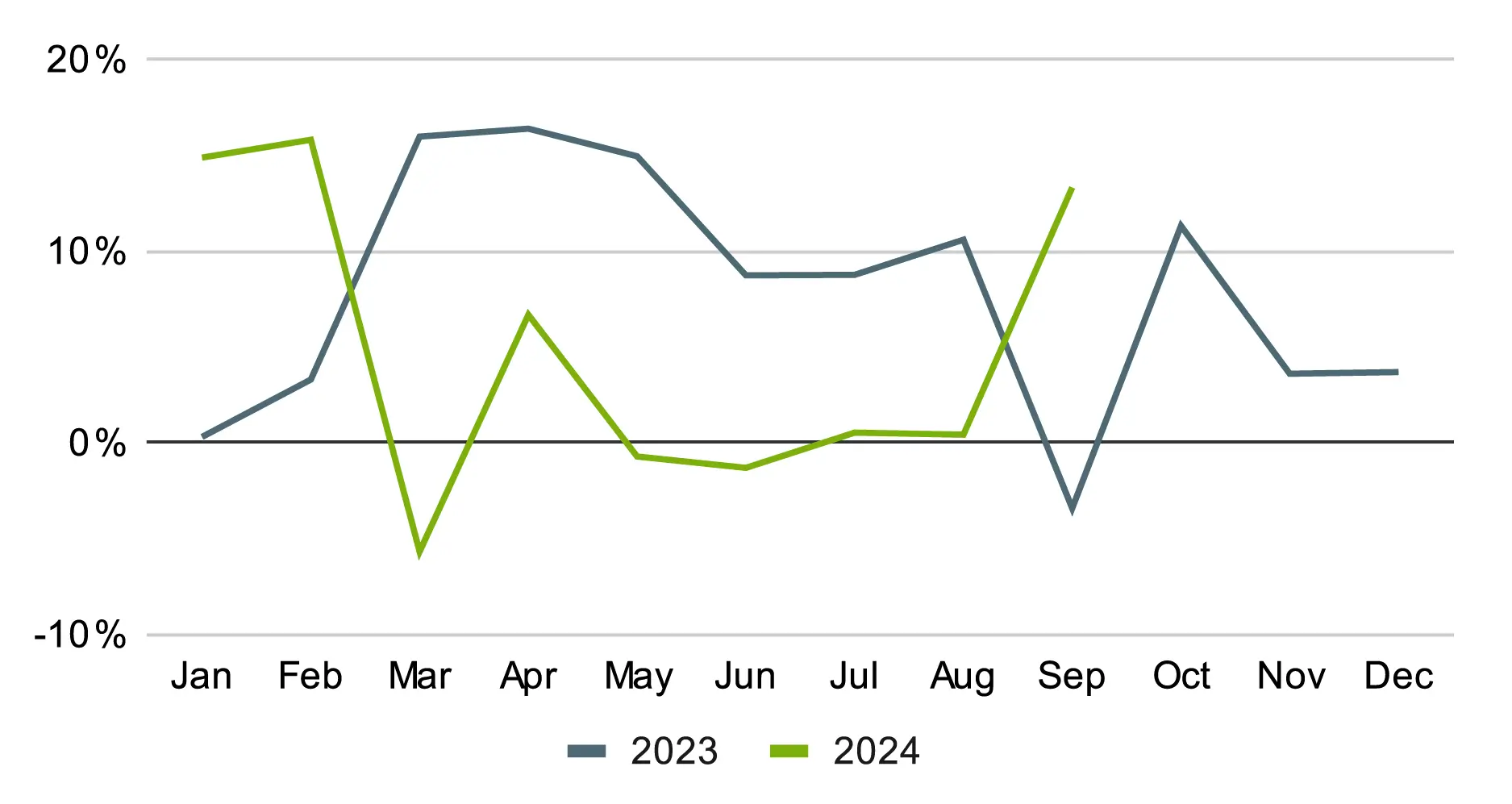

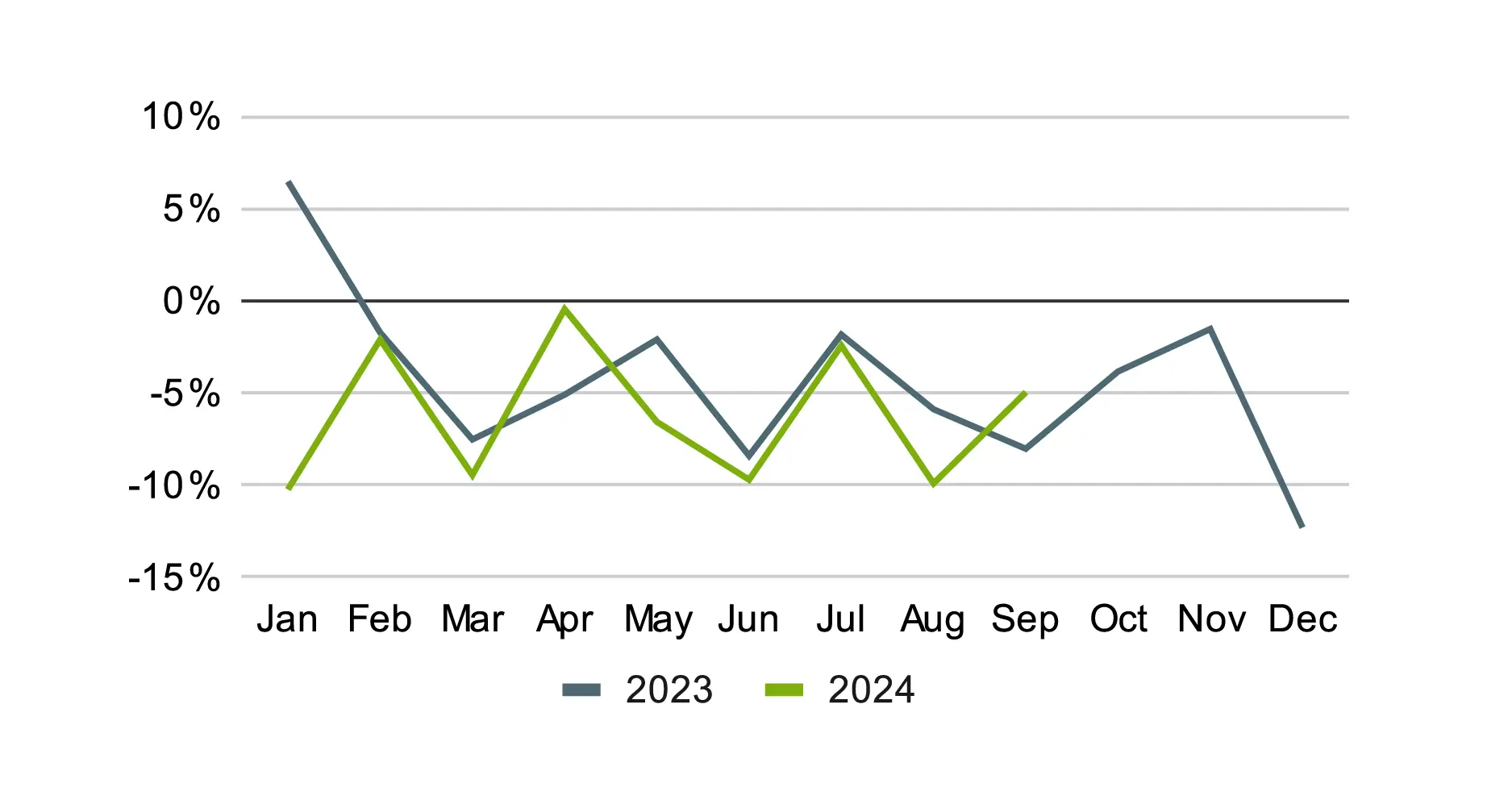

Construction services include businesses in residential and commercial construction, remodeling, and related industries. In line with the views on consumer spending, median revenue is showing signs of improvement, likely due to consumer spending leaning towards maintenance and improvements. The continued decline in new work scheduled during Q3 reflects caution around spending as the economic recovery gains momentum.

New Work Scheduled YoY — Construction

Median Revenue YoY — Construction

Future Outlook

The Q3 2024 Jobber Home Service Economic Report highlights a promising outlook for the home services sector as interest rate cuts begin to boost consumer spending and demand. Rising home equity and a shift toward maintenance projects are expected to drive steady growth, especially as financial conditions continue to improve. The sector is well-positioned to benefit from an aging housing stock and an increased focus on essential updates, setting the stage for sustained demand and expansion through 2025 and beyond.

Methodology & Data Sources

- The small business data provided is sourced from the FAQ section of the U.S. Small Business Administration Office of Advocacy.

- The consumer spending data was sourced from The Bureau of Economic Analysis.

- The Real Disposable Personal Income data and chart is sourced from the Federal Reserve Bank of St. Louis.

- The Index of Consumer Sentiment was sourced from Surveys of Consumers by the University of Michigan.

- The Home Equity Values data and chart were sourced from the Federal Reserve Bank of St. Louis.

- The average 30 yr fixed mortgage rates were sourced from the Federal Reserve Bank of St. Louis

- The monthly construction data and chart were sourced from the United States Census Bureau: Construction Spending.

- The new permits data and chart were sourced from the United States Census Bureau: New Residential Construction.

- The new housing starts data and chart were sourced from the United States Census Bureau: Monthly New Residential Construction, June 2024.

- The Leading Indicator of Remodeling Activity data and chart are sourced from The Joint Center for Housing Studies of Harvard.

- The year-over-year change in median revenue, new work scheduled, and invoice sizes were calculated by aggregating data from a cohort of businesses using Jobber since January 2021. This doesn’t include any new businesses that started using Jobber during that period.